Back

BackDiscrete and Continuous Random Variables, Probability Distributions, and the Normal Distribution

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Discrete Random Variables

Definition and Examples

A discrete random variable is a variable whose possible values are countable and arise from the outcome of a random experiment. Examples include the number of boys in a family, the number of defective light bulbs in a box, or the number of customers arriving at a bank within a given time period. These values are finite or countably infinite and can be listed out.

Random Variable: A numerical value generated by a random experiment.

Discrete Random Variable: Takes on countable values (e.g., 0, 1, 2, ...).

Continuous Random Variable: Takes on values in a continuous interval (see below).

Probability Distributions for Discrete Random Variables

The probability distribution of a discrete random variable X is a list of each possible value of X together with the probability that X takes that value in one trial of the experiment. The probabilities must satisfy two conditions:

Each probability P(x) must be between 0 and 1:

The sum of all possible probabilities is 1:

Continuous Random Variables

Definition and Properties

A continuous random variable is one whose set of possible values contains a whole interval of decimal numbers. For such variables, the probability that X assumes any single particular value is zero; instead, probabilities are assigned to intervals of values.

Examples: Heights of people, time until an event occurs, weights of objects.

Probabilities are calculated over intervals, not at specific points.

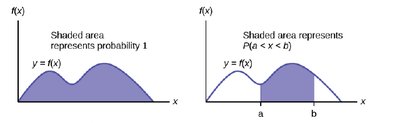

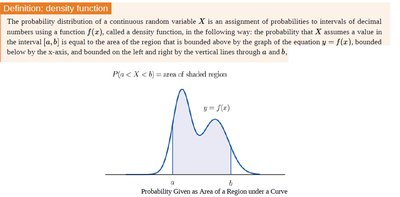

Probability Distributions for Continuous Random Variables

The probability distribution of a continuous random variable X is described by a density function f(x). The probability that X assumes a value in the interval [a, b] is equal to the area under the curve of f(x) from a to b:

The total area under the density curve is 1.

Common Continuous Distributions

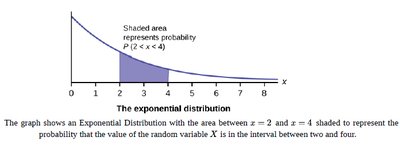

Exponential Distribution: Models the time between events in a Poisson process. The probability that X is between two values is the area under the curve between those values.

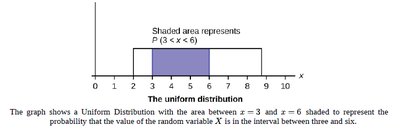

Uniform Distribution: All intervals of the same length within the distribution's range are equally probable.

The Normal Distribution

Definition and Formula

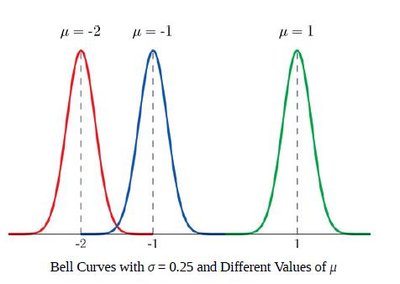

The normal distribution is a continuous probability distribution that is symmetric and bell-shaped. It is defined by two parameters: the mean (μ) and the standard deviation (σ). The probability density function is:

μ determines the center (location) of the curve.

σ determines the spread (width) of the curve.

Properties of the Normal Distribution

The curve is symmetric about the mean μ.

The total area under the curve is 1.

The mean, median, and mode are all equal.

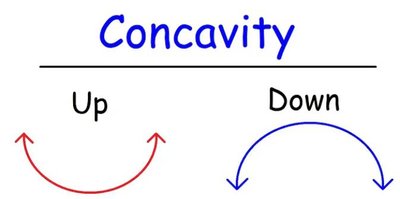

Inflection points occur at μ ± σ, where the curve changes concavity.

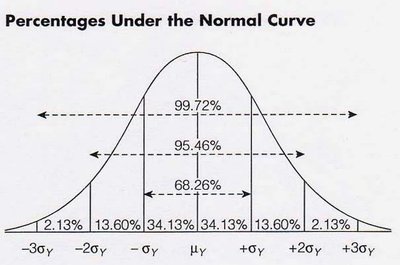

The Empirical Rule (68-95-99.7 Rule)

The empirical rule describes the percentage of data within certain standard deviations from the mean in a normal distribution:

About 68% of values lie within 1 standard deviation (μ ± σ).

About 95% of values lie within 2 standard deviations (μ ± 2σ).

About 99.7% of values lie within 3 standard deviations (μ ± 3σ).

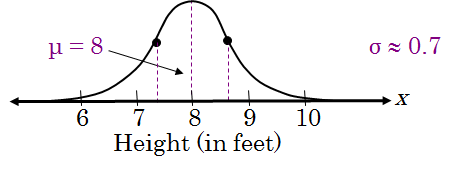

Interpreting Normal Curves

Given a normal curve, the mean is the center of symmetry, and the standard deviation can be estimated by the distance from the mean to the inflection points.

Example: If the mean height of magnolia bushes is 8 feet and the inflection points are at 7.3 and 8.7, then σ ≈ 0.7 feet.

Standard Normal Distribution and Z-Scores

Standard Normal Distribution

The standard normal distribution is a normal distribution with mean μ = 0 and standard deviation σ = 1. Any normal random variable X can be converted to a standard normal variable Z using the transformation:

Z-scores measure how many standard deviations a value is from the mean.

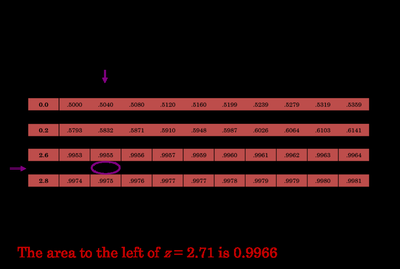

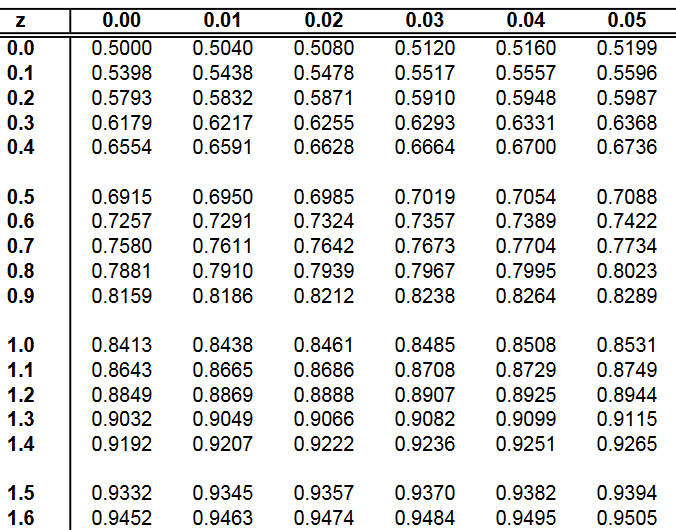

Using the Standard Normal Table

The cumulative standard normal table gives the area (probability) to the left of a given z-score. To find probabilities:

For P(Z < z), read the table directly.

For P(Z > z), compute 1 - P(Z < z).

For P(a < Z < b), compute P(Z < b) - P(Z < a).

Finding Probabilities for Normal Distributions

To find the probability that a normal random variable X falls within a certain interval:

Convert the X values to Z-scores using .

Use the standard normal table to find the corresponding area (probability).

Example: If X ~ N(500, 100), P(X < 600) = P(Z < 1) = 0.8413.

Finding Values Given Probabilities (Percentiles)

To find the value x corresponding to a given percentile (area to the left):

Find the z-score corresponding to the desired area using the standard normal table.

Transform back to the original scale: .

Example: For the top 5% (95th percentile), find z ≈ 1.645, then compute x.

Summary Table: Key Properties of Discrete vs. Continuous Random Variables

Property | Discrete Random Variable | Continuous Random Variable |

|---|---|---|

Possible Values | Countable (finite or infinite) | Any value in an interval |

Probability at a Point | P(X = x) > 0 | P(X = x) = 0 |

Probability Calculation | Sum of probabilities | Area under density curve |

Total Probability | Total area = 1 |

Additional info: This guide covers foundational concepts for understanding probability distributions, including the normal distribution, which is central to inferential statistics and hypothesis testing.